Understanding Japanese Public Health Insurance & Private Medical Insurance for Foreigners in Japan (And Why to Combine Them)

Learn how Japan’s public health insurance and private medical insurance work for foreign residents, and why combining both can be the key to better healthcare coverage and financial security in Japan.

CONTENTS

Public Health Insurance vs Private Health Insurance in Japan

Moving to Japan, there’s so much to look forward to, but also so much to prepare! When it comes to Japan’s public health insurance, though, it’s worth giving your situation a serious look, whether you’re a new arrival or you’ve been here for years.

Japan has a universal healthcare system, and residents staying longer than three months are required to either sign up for public medical insurance (Japan’s National Health Insurance or health insurance provided by an employer). That means enrolling in public health insurance is one of the first major administrative tasks required of many foreigners living in Japan. In the long term, however, it’s not unusual for foreign residents to discover that public health insurance doesn’t cut it.

▶︎ Found an English teaching job as a “contractor”? Having steady work and public health insurance (or employer-provided health insurance) might seem like enough, but what happens when you get into a bike accident or come down with something nasty enough to keep you away from work? What’s going to keep you afloat and ahead of daily expenses if you’re in the hospital?

▶︎ Maybe you felt a strange twinge that you need a doctor to investigate? Japan’s medical system is all in Japanese, and if you’re new to the country, you might be hard-pressed to find reliable help as you navigate the system in another language.

As foreign residents, public health insurance isn’t always enough to address our healthcare needs, especially when it comes to hospitalization costs, language support, or financial protection during serious illness.

This is where private medical insurance enters the picture. Private insurers offer insurance plans designed to supplement the public health insurance system. And Nanairo Life, a well-known Japanese insurer, has plans made for foreign residents of Japan, with English support.

When you’re far from your most trusted friends and family, private medical insurance can come to your rescue in a number of different ways: helping to bear the financial burden when you’re sick and in need (in the form of hospitalization benefits), or finding you healthcare advice (via English support lines).

In the end, it’s especially important for foreign residents (just like all of us on the Japankuru team) to understand what parts are played by Japanese public health insurance and private medical insurance plans, because knowing what each system provides can make a major difference in your medical and financial peace of mind while living long-term in Japan.

What Is Japan’s National Health Insurance? Do You Need It?

Japan’s National Health Insurance, often referred to as “NHI” or the Japanese “Kokumin Kenko Hoken,” is one pillar of the country’s universal healthcare program. Foreign residents staying in Japan longer than three months need to know that enrollment is generally required, unless they are already covered by an employer-sponsored plan. NHI is administered by local municipalities, meaning enrollment and premium calculations are handled by city or ward offices—the exact premiums vary depending on your previous year’s income, household size, and municipality.

▶︎ For English teachers in particular, many contract workers don’t have employer-provided health insurance, which means enrolling in NHI is common.

What NHI Covers & Where It Falls Short

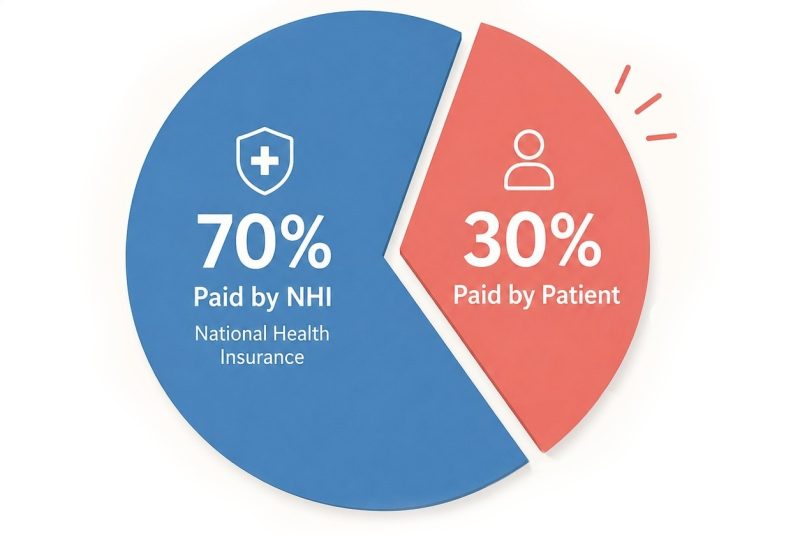

By international standards, Japan’s National Health Insurance can feel fairly comprehensive, and coverage generally includes doctor visits, hospital treatment/surgery, dental, mental health care, and prescription medication. For all of these costs, insurance typically pays around 70% of approved medical costs, while patients pay the remaining 30% out of pocket.

Despite its strong coverage, NHI has limitations. Many preventive screenings are typically excluded, as well as certain advanced treatments or elective procedures, and things like cosmetic procedures or private hospital rooms. If you’re planning to settle down long-term in Japan, you might be surprised at how many things seem to be lacking! Even when NHI does reduce health costs significantly, serious hospitalization can still create financial strain through lost income, transportation costs, uncovered treatments, or extended recovery periods.

Another challenge many foreign residents face is that Japan’s public healthcare system is clearly not designed for non-Japanese speakers, and practical healthcare communication—booking appointments, understanding diagnoses, dealing with billing, even medication instructions—can be difficult for foreign residents. With all the medical jargon, a trip to the doctor can be stressful even for those with a grasp of everyday Japanese. It’s one major reason why many foreign residents look to private insurance providers, able to provide better linguistic support.

What Is Private Medical Insurance in Japan? How Does It Work?

In Japan, private insurers provide medical insurance as a supplement to NHI, like the handful of different plans offered by Nanairo Life. These plans provide additional financial protection to cover the costs of hospitalization and surgery resulting from illness or injury. Depending on the plan, that can include major medical crises like cancer, heart attack, or stroke.

Coverage can vary a lot from one insurance company to another, but Nanairo’s is well equipped to support foreign residents, with simple plans, affordable premiums, and extensive English-language assistance. Get insured through Nanairo Life, and not only can you apply in English, but you can also use the English-language support service. Policyholders gain access to telephone support, available in English and Chinese, offering help with everything from finding the right doctor to everyday medical worries. Burned your hand on the stove? Worried about your kid’s sudden fever? Struggling with new seasonal allergies? Not sure what to do here in Japan? It’s nice to have somebody who can help you find the right answers in English (or Chinese)!

Adding Japanese Private Medical Insurance: Insurance From Nanairo Life

Private medical insurance varies by plan, but medical insurance like the kind offered by Nanairo Life typically focuses on hospitalization, surgery, or outpatient benefits, lump-sum payouts after diagnosis, income protection during illness, and other additional cash benefits beyond public insurance. Premiums tend to be surprisingly affordable, starting at around 1,000 yen a month—the price of a couple cups of coffee. You’re probably already spending that much when you pay the import price for your favorite snacks from back home.

One key point is that, while public health insurance pays healthcare providers, private medical insurers generally pay benefits directly to the insured person: you. That means you’re free to use the money for anything—making up for lost wages, covering remaining treatment costs, rent, travel expenses—whatever you actually need it for at that moment. Looking at it practically, if you somehow end up in the hospital for several weeks, public health insurance may limit the financial load of the medical bill, but Nanairo can provide the timely cash infusions you need to offset any financial burdens. Even if you can’t tutor your students, show up for your part-time job at the local yakiniku shop, or go in for regular work hours.

Nanairo has a couple of insurance plans targeting specific diseases, and plenty of customization options, but they also keep things simple with a few basic medical insurance plans. The main one is Nanairo Medical Ishizue, which is for all ages (0–85), and anyone 18 or older can easily apply online for coverage that includes hospitalization and outpatient care, lump-sum payment for certain major diseases, and premiums that never increase.

If you’re particularly worried about pre-existing conditions, Nanairo Medical Super Wide is the simplest option, because the application process includes just two health questions! (It’s available for those aged 20-85.)

Why Foreign Residents Often Choose Both Public Health Insurance & Private Medical Insurance

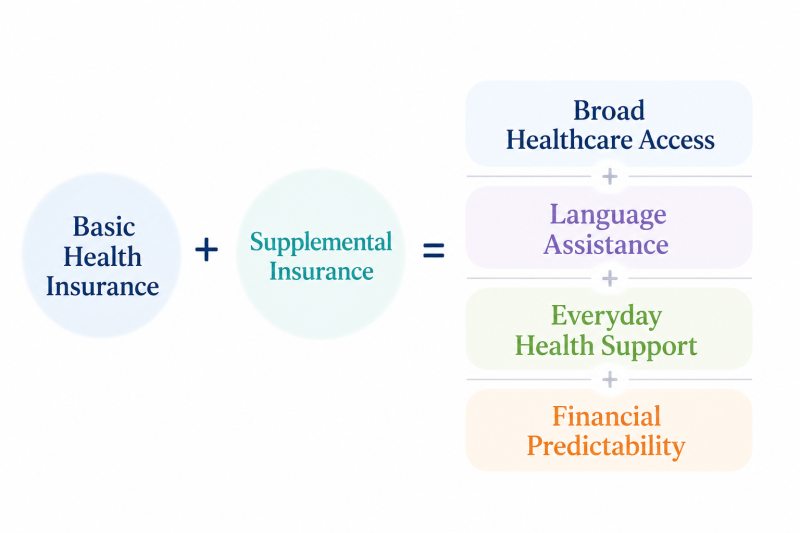

For foreign residents, one key point is that public health insurance and private medical insurance in Japan are not really competing systems, since they serve different purposes. National Health Insurance, or the alternatives provided by some employers, offer access to the Japanese healthcare system. But private medical insurance companies like Nanairo exist to keep you better covered.

Public health insurance may cover 70% of a surgery, but the patient is still left paying 30% of the costs, which can be a hefty sum. Private insurance hospitalization benefits can help cover the remaining portion, and offer additional payouts to compensate for missed work or recovery expenses. For a multi-layered approach to healthcare, adding a private health insurance plan helps to cover any holes, so it’s actually fairly common among Japanese citizens, and increasingly popular among foreign residents in Japan.

For foreign residents, in particular, there are additional reasons to consider supplemental insurance:

1. Language Assistance: Generally speaking, Japanese is required to communicate with Japanese private insurance companies, which adds extra stress during emergencies. Nanairo Life’s English-speaking support can simplify application and insurance claim procedures.

2. Everyday Health Support: When you’re in another country, it’s hard to know where to turn when you’re tackling health-related issues. Nanairo offers additional English-language support services for policyholders, where the helpful staff can help you figure out exactly what to do next.

3. Financial Predictability: Serious illness can affect income stability, especially for the many foreign freelancers, language teachers, or other self-employed residents in Japan who lack employer benefits. Nanairo Life’s medical insurance plans can take away a little of that uncertainty, with monthly premiums as low as around 1,000 yen a month. For newcomers unfamiliar with the Japanese system, supplemental insurance can also reduce any worries you may have about unexpected costs.

What Kind of Japanese Medical Insurance Is Right For You?

When you first arrive in Japan, it can be hard to get a good grasp of Japan’s healthcare system, let alone nailing down exactly what kind of coverage you need when it comes to Japanese health insurance. But in the end, for most foreign residents in Japan, the answers are straightforward: public health insurance (NHI or employer-provided insurance) is essential, but private medical insurance can be a valuable addition for a wide variety of residents.

Whether you’re a young professional trying out English teaching in a new country, an exchange student working hard on your Japanese, or a parent picking up and moving the whole family to Japan for a new job… if you’re a foreign resident trying to settle into Japan, you need to consider your insurance options.

Japan’s healthcare system may be regarded as accessible and cost-effective, but the supplemental health coverage provided by companies like Nanairo Life provides an additional safety net, particularly for foreigners concerned about hospitalization costs, language barriers, or all the ways an illness could turn life upside down.

Ultimately, the right combination depends on you and your family’s needs, but for many long-term foreign residents, combining Japan’s public health insurance with private medical insurance coverage can provide the right balance of affordability, access, and security. If you want to find out more about Nanairo’s insurance plans, you can find all the details on the official Nanairo Life website.

For more info and updates from Japan, check Japankuru for new articles, and don’t forget to follow us on X (Twitter), Instagram, and Facebook!

COMMENT

FEATURED MEDIA

VIEW MORE

A New Tokyo Animal Destination: Relax & Learn About the World’s Animals in Japan

#pr #japankuru #anitouch #anitouchtokyodome #capybara #capybaracafe #animalcafe #tokyotrip #japantrip #카피바라 #애니터치 #아이와가볼만한곳 #도쿄여행 #가족여행 #東京旅遊 #東京親子景點 #日本動物互動體驗 #水豚泡澡 #東京巨蛋城 #เที่ยวญี่ปุ่น2025 #ที่เที่ยวครอบครัว #สวนสัตว์ในร่ม #TokyoDomeCity #anitouchtokyodome

Shohei Ohtani Collab Developed Products & Other Japanese Drugstore Recommendations From Kowa

#pr #japankuru

#kowa #syncronkowa #japanshopping #preworkout #postworkout #tokyoshopping #japantrip #일본쇼핑 #일본이온음료 #오타니 #오타니쇼헤이 #코와 #興和 #日本必買 #日本旅遊 #運動補充能量 #運動飲品 #ช้อปปิ้งญี่ปุ่น #เครื่องดื่มออกกำลังกาย #นักกีฬา #ผลิตภัณฑ์ญี่ปุ่น #อาหารเสริมญี่ปุ่น

도쿄 근교 당일치기 여행 추천! 작은 에도라 불리는 ‘가와고에’

세이부 ‘가와고에 패스(디지털)’ 하나면 편리하게 이동 + 가성비까지 완벽하게! 필름카메라 감성 가득한 레트로 거리 길거리 먹방부터 귀여움 끝판왕 핫플&포토 스폿까지 총집합!

Looking for day trips from Tokyo? Try Kawagoe, AKA Little Edo!

Use the SEIBU KAWAGOE PASS (Digital) for easy, affordable transportation!

Check out the historic streets of Kawagoe for some great street food and plenty of picturesque retro photo ops.

#pr #japankuru #도쿄근교여행 #가와고에 #가와고에패스 #세이부패스 #기모노체험 #가와고에여행 #도쿄여행코스 #도쿄근교당일치기 #세이부가와고에패스

#tokyotrip #kawagoe #tokyodaytrip #seibukawagoepass #kimono #japantrip

Hirakata Park, Osaka: Enjoy the Classic Japanese Theme Park Experience!

#pr #japankuru #hirakatapark #amusementpark #japantrip #osakatrip #familytrip #rollercoaster #retrôvibes #枚方公園 #大阪旅遊 #關西私房景點 #日本親子旅行 #日本遊樂園 #木造雲霄飛車 #히라카타파크 #สวนสนุกฮิราคาตะพาร์ค

🍵Love Matcha? Upgrade Your Matcha Experience With Tsujiri!

・160년 전통 일본 말차 브랜드 츠지리에서 말차 덕후들이 픽한 인기템만 골라봤어요

・抹茶控的天堂!甜點、餅乾、飲品一次滿足,連伴手禮都幫你列好清單了

・ส่องมัทฉะสุดฮิต พร้อมพาเที่ยวร้านดังในอุจิ เกียวโต

#pr #japankuru #matcha #matchalover #uji #kyoto #japantrip #ujimatcha #matchalatte #matchasweets #tsujiri #말차 #말차덕후 #츠지리 #교토여행 #말차라떼 #辻利抹茶 #抹茶控 #日本抹茶 #宇治 #宇治抹茶 #日本伴手禮 #抹茶拿鐵 #抹茶甜點 #มัทฉะ #ของฝากญี่ปุ่น #ชาเขียวญี่ปุ่น #ซึจิริ #เกียวโต

・What Is Nenaito? And How Does This Sleep Care Supplement Work?

・你的睡眠保健品——認識「睡眠茶氨酸錠」

・수면 케어 서플리먼트 ‘네나이토’란?

・ผลิตภัณฑ์เสริมอาหารดูแลการนอน “Nenaito(ネナイト)” คืออะไร?

#pr #japankuru #sleepcare #japanshopping #nenaito #sleepsupplement #asahi #睡眠茶氨酸錠 #睡眠保健 #朝日 #l茶胺酸 #日本藥妝 #日本必買 #일본쇼핑 #수면 #건강하자 #네나이토 #일본영양제 #อาหารเสริมญี่ปุ่น #ช้อปปิ้งญี่ปุ่น #ร้านขายยาญี่ปุ่น #ดูแลตัวเองก่อนนอน #อาซาฮิ

Japanese Drugstore Must-Buys! Essential Items from Hisamitsu® Pharmaceutical

#PR #japankuru #hisamitsu #salonpas #feitas #hisamitsupharmaceutical #japanshopping #tokyoshopping #traveltips #japanhaul #japantrip #japantravel

Whether you grew up with Dragon Ball or you just fell in love with Dragon Ball DAIMA, you'll like the newest JINS collab. Shop this limited-edition Dragon Ball accessory collection to find some of the best Dragon Ball merchandise in Japan!

>> Find out more at Japankuru.com! (link in bio)

#japankuru #dragonball #dragonballdaima #animecollab #japanshopping #jins #japaneseglasses #japantravel #animemerch #pr

This month, Japankuru teamed up with @official_korekoko to invite three influencers (originally from Thailand, China, and Taiwan) on a trip to Yokohama. Check out the article (in Chinese) on Japankuru.com for all of their travel tips and photography hints - and look forward to more cool collaborations coming soon!

【橫濱夜散策 x 教你怎麼拍出網美照 📸✨】

每次來日本玩,是不是都會先找旅日網紅的推薦清單?

這次,我們邀請擁有日本豐富旅遊經驗的🇹🇭泰國、🇨🇳中國、🇹🇼台灣網紅,帶你走進夜晚的橫濱!從玩樂路線到拍照技巧,教你怎麼拍出最美的夜景照。那些熟悉的景點,換個視角說不定會有新發現~快跟他們一起出發吧!

#japankuru #橫濱紅磚倉庫 #汽車道 #中華街 #yokohama #japankuru #橫濱紅磚倉庫 #汽車道 #中華街 #yokohama #yokohamaredbrickwarehouse #yokohamachinatown

If you’re a fan of Vivienne Westwood's Japanese designs, and you’re looking forward to shopping in Harajuku this summer, we’ve got important news for you. Vivienne Westwood RED LABEL Laforet Harajuku is now closed for renovations - but the grand reopening is scheduled for July!

>> Find out more at Japankuru.com! (link in bio)

#japankuru #viviennewestwood #harajuku #omotesando #viviennewestwoodredlabel #viviennewestwoodjapan #비비안웨스트우드 #오모테산도 #하라주쿠 #日本購物 #薇薇安魏斯伍德 #日本時尚 #原宿 #表參道 #japantrip #japanshopping #pr

Ready to see TeamLab in Kyoto!? At TeamLab Biovortex Kyoto, the collective is taking their acclaimed immersive art and bringing it to Japan's ancient capital. We can't wait to see it for ourselves this autumn!

>> Find out more at Japankuru.com! (link in bio)

#japankuru #teamlab #teamlabbiovortex #kyoto #kyototrip #japantravel #artnews

Photos courtesy of teamLab, Exhibition view of teamLab Biovortex Kyoto, 2025, Kyoto ® teamLab, courtesy Pace Gallery

MAP OF JAPAN

SEARCH BY REGION

-

-

HOKKAIDO

VIEW MORE

Hokkaido (北海道) is the northernmost of the four main islands that make up Japan. The area is famous for Sapporo Beer, plus brewing and distilling in general, along with fantastic snow festivals and breathtaking national parks. Foodies should look for Hokkaido's famous potatoes, cantaloupe, dairy products, soup curry, and miso ramen!

-

NIKI

VIEW MORE

Niki, in south-west Hokkaido, is about 30 minutes from Otaru. The small town is rich with natural resources, fresh water, and clean air, making it a thriving center for fruit farms. Cherries, tomatoes, and grapes are all cultivated in the area, and thanks to a growing local wine industry, it's quickly becoming a food and wine hotspot. Together with the neighboring town of Yoichi, it's a noted area for wine tourism.

-

NISEKO

VIEW MORE

Niseko is about two hours from New Chitose Airport, in the western part of Hokkaido. It's one of Japan's most noted winter resort areas, and a frequent destination for international visitors. That's all because of the super high-quality powder snow, which wins the hearts of beginners and experts alike, bringing them back for repeat visits. That's not all, though, it's also a great place to enjoy Hokkaido's culinary scene and some beautiful onsen (hot springs).

-

OTARU

VIEW MORE

Otaru is in western Hokkaido, about 30 minutes from Sapporo Station. The city thrived around its busy harbor in the 19th and 20th centuries thanks to active trade and fishing, and the buildings remaining from that period are still popular attractions, centered around Otaru Canal. With its history as a center of fishing, it's no surprise that the area's fresh sushi is a must-try. Otaru has over 100 sushi shops, quite a few of which are lined up on Sushiya Dori (Sushi Street).

-

SAPPORO

VIEW MORE

Sapporo, in the south-western part of Hokkaido, is the prefecture's political and economic capital. The local New Chitose Airport see arrivals from major cities like Tokyo and Osaka, alongside international flights. Every February, the Sapporo Snow Festival is held in Odori Park―one of the biggest events in Hokkaido. It's also a hotspot for great food, known as a culinary treasure chest, and Sapporo is a destination for ramen, grilled mutton, soup curry, and of course Hokkaido's beloved seafood.

-

-

-

TOHOKU

VIEW MORE

Consisting of six prefectures, the Tohoku Region (東北地方) is up in the northeastern part of Japan's main island. It's the source of plenty of the nation's agriculture (which means great food), and packed with beautiful scenery. Explore the region's stunning mountains, lakes, and hot springs!

-

AKITA

VIEW MORE

Akita Prefecture is on the Sea of Japan, in the northern reaches of Japan's northern Tohoku region. Akita has more officially registered important intangible culture assets than anywhere else in Japan, and to this day visitors can experience traditional culture throughout the prefecture, from the Oga Peninsula's Namahage (registered with UNESCO as a part of Japan's intangible cultural heritage), to the Tohoku top 3 Kanto Festival. Mysterious little spots like the Oyu Stone Circle Site and Ryu no Atama (Dragon's Head) are also worth a visit!

-

FUKUSHIMA

VIEW MORE

Fukushima Prefecture sits at the southern tip of Japan's northern Tohoku region, and is divided into three parts with their own different charms: the Coastal Area (Hama-dori), the Central Area (Naka-dori), and the Aizu Area. There's Aizu-Wakamatsu with its Edo-era history and medieval castles, Oze National Park, Kitakata ramen, and Bandai Ski Resort (with its famous powder snow). Fukushima is a beautiful place to enjoy the vivid colors and sightseeing of Japan's beloved four seasons.

-

YAMAGATA

VIEW MORE

Yamagata Prefecture is up against the Sea of Japan, in the southern part of the Tohoku region, and it's especially popular in winter, when travelers soak in the onsen (hot springs) and ski down snowy slopes. International skiiers are especially fond of Zao Onsen Ski Resort and Gassan Ski Resort, and in recent years visitors have been drawn to the area to see the mystical sight of local frost-covered trees. Some destinations are popular regardless of the season, like Risshakuji Temple, AKA Yamadera, Ginzan Onsen's nostalgic old-fashioned streets, and Zao's Okama Lake, all great for taking pictures. Yamagata is also the place to try Yonezawa beef, one of the top 3 varieties of wagyu beef.

-

-

-

KANTO

VIEW MORE

Japan's most densely populated area, the Kanto Region (関東地方) includes 7 prefectures: Gunma, Tochigi, Ibaraki, Saitama, Tokyo, Chiba, and Kanagawa, which means it also contains the Tokyo Metropolitan Area. In modern-day Japan, Kanto is the cultural, political, and economic heartland of the country, and each prefecture offers something a little different from its neighbors.

-

GUNMA

VIEW MORE

Gunma Prefecture is easily accessible from Tokyo, and in addition to the area's popular natural attractions like Oze Marshland and Fukiware Falls, Gunma also has a number of popular hot springs (Kusatsu, Ikaho, Minakami, Shima)―it's even called an Onsen Kingdom. The prefecture is popular with history buffs and train lovers, thanks to spots like world heritage site Tomioka Silk Mill, the historic Megane-bashi Bridge, and the Watarase Keikoku Sightseeing Railway.

-

TOCHIGI

VIEW MORE

Tochigi Prefecture's capital is Utsunomiya, known for famous gyoza, and just an hour from Tokyo. The prefecture is full of nature-related sightseeing opportunities year-round, from the blooming of spring flowers to color fall foliage. Tochigi also has plenty of extremely well-known sightseeing destinations, like World Heritage Site Nikko Toshogu Shrine, Lake Chuzenji, and Ashikaga Flower Park―famous for expansive wisteria trellises. In recent years the mountain resort town of Nasu has also become a popular excursion, thanks in part to the local imperial villa. Tochigi is a beautiful place to enjoy the world around you.

-

TOKYO

VIEW MORE

Tokyo (東京) is Japan's busy capital, and the most populous metropolitan area in the world. While the city as a whole is quite modern, crowded with skyscrapers and bustling crowds, Tokyo also holds onto its traditional side in places like the Imperial Palace and Asakusa neighborhood. It's one of the world's top cities when it comes to culture, the arts, fashion, games, high-tech industries, transportation, and more.

-

-

-

CHUBU

VIEW MORE

The Chubu Region (中部地方) is located right in the center of Japan's main island, and consists of 9 prefectures: Aichi, Fukui, Gifu, Ishikawa, Nagano, Niigata, Shizuoka, Toyama, and Yamanashi. It's primarily famous for its mountains, as the region contains both Mt. Fuji and the Japanese Alps. The ski resorts in Niigata and Nagano also draw visitors from around the world, making it a popular winter destination.

-

NAGANO

VIEW MORE

Nagano Prefecture's popularity starts with a wealth of historic treasures, like Matsumoto Castle, Zenkoji Temple, and Togakushi Shrine, but the highlight might just be the prefecture's natural vistas surrounded by the "Japanese Alps." Nagano's fruit is famous, and there are plenty of places to pick it fresh, and the area is full of hot springs, including Jigokudani Monkey Park―where monkeys take baths as well! Thanks to the construction of the Hokuriku shinkansen line, Nagano is easily reachable from the Tokyo area, adding it to plenty of travel itineraries. And after the 1998 Nagano Winter Olympics, ski resorts like Hakuba and Shiga Kogen are known around the world.

-

NAGOYA

VIEW MORE

Aichi Prefecture sits in the center of the Japanese islands, and its capital city, Nagoya, is a center of politics, commerce, and culture. While Aichi is home to major industry, and is even the birthplace of Toyota cars, it's proximity to the sea and the mountains means it's also a place with beautiful natural scenery, like Saku Island, Koijigahama Beach, Mt. Horaiji. Often used a stage for major battles in Japanese history, Sengoku era commanders like Oda Nobunaga, Toyotomi Hideyoshi, and Tokugawa Ieyasu left their own footprints on Aichi, and historic buildings like Nagoya Castle, Inuyama Castle, and those in Meiji Mura are still around to tell the tale.

-

NIIGATA

VIEW MORE

Niigata is a prefecture on Japan's main island of Honshu, situated right on the coast of the Sea of Japan, and abundant with the gifts of nature. It's known for popular ski resorts such as Echigo-Yuzawa, Japanese national parks, and natural hot spring baths, plus local products like fresh seafood, rice, and sake. Visitors often spend time in the prefectural capital, Niigata City, or venture across the water to Sado Island.

-

SHIZUOKA

VIEW MORE

Shizuoka Prefecture is sandwiched between eastern and western Japan, giving the prefecture easy access to both Tokyo and Osaka. Not only is it known for beautiful natural attractions, with everything from Mount Fuji to Suruga Bay, Lake Hamanako, and Sumata Pass―Shizuoka's Izu Peninsula is known as a go-to spot for hot springs lovers, with famous onsen like Atami, Ito, Shimoda, Shuzenji, and Dogashima. Shizuoka attracts all kinds of travelers thanks to historic connections with the Tokugawa clan, the Oigawa Railway, fresh eel cuisine, Hamamatsu gyoza, and famously high-quality green tea.

-

-

-

KANSAI

VIEW MORE

Kansai (関西) is a region that includes Mie, Nara, Wakayama, Kyoto, Osaka, Hyogo, and Shiga Prefectures. Kansai contained Japan's ancient capital for hundreds of years, and it's making a comeback as one of the most popular parts of Japan. Kyoto's temples and shrines, Osaka Castle, and the deer of Nara are all considered must-sees. Plus, the people of Kansai are especially friendly, making it a fun place to hang out.

-

KYOTO

VIEW MORE

Kyoto flourished as the capital of Japan between the years 794 and 1100, becoming a center for poilitics and culture, and to this day it's a great place for close encounters with Japanese history. The cobbled streets of Gion, the atmospheric road to Kiyomizudera Temple, Kinkakuji's golden walls and countless historic attractions, even Arashiyama's Togetsukyo Bridge―Kyoto is a place of many attractions. With new charms to experience throughout the seasons, travelers can't stop themselves from returning again and again.

-

NARA

VIEW MORE

Nara Prefecture's important history reaches back to 710, a time now called the Nara era, when it was once capital of Japan. Called "Heijo-kyo" during its time as a capital, it's said that nara was once the end of the silk road, leading it to flourish as a uniquely international region and produce important cultural properties of all kinds. To make the most of each season, travelers head to Nara Park, where the Nara deer who wander freely, or climb Mount Yoshino, a famous cherry blossom spot.

-

OSAKA

VIEW MORE

Osaka is known for friendly (and funny) people, but its history is nothing to laugh at, playing a major part in Toyotomi Hideyoshi's 16th century unification of Japan. Thanks to long years of economic activity, it's one of Japan's biggest cities, and Osaka's popular food culture earned it the nickname "The Kitchen of the Nation." To this day Osaka is the model of western Japan, and alongside historic structures like Osaka Castle, it also has major shopping malls like Umeda's Grand Front Osaka and Tennoji's Abeno Harukas. Osaka is a place to eat, eat, eat, with local specialties like takoyaki, okonomiyaki, and kushi-katsu, and for extra fun, it's home to Universal Studios Japan.

-

-

-

CHUGOKU

VIEW MORE

The Chugoku Region (中国地方) consists of five prefectures: Hiroshima, Okayama, Shimane, Tottori, and Yamaguchi. In Chugoku you’ll find the sand dunes of Tottori, and Hiroshima’s atomic bomb site, plus centers of ancient history like Grand Shrine of Izumo.

-

HIROSHIMA

VIEW MORE

Hiroshima Prefecture has everything, from world heritage sites to beautiful nature and delicious local cuisine, and it's either an hour and a half from Tokyo by plane, or four hours by train. Itsukushima Shrine on Miyajima Island and the Atomic Bomb Dome, two Hiroshima UNESCO sites, are famous around the world, but in Japan it's also famous for food. Seafood from the Seto Inland Sea, especially oysters, Hiroshima-style okonomiyaki, and Setouchi lemons are all popular, and the natural scenery alone is worth seeing.

-

-

-

SHIKOKU

VIEW MORE

On the other side of the Seto Inland Sea opposite Japan’s main island, Shikoku (四国) is a region made up of four prefectures: Ehime, Kagawa, Kochi, and Tokushima. The area is famous for its udon (in Kagawa), and the beautiful Dogo Onsen hot springs (in Ehime).

-

KAGAWA

VIEW MORE

Kagawa Prefecture is on the northern part of the island of Shikoku, facing Japan's main island and the Seto Inland Sea. It's known for being the smallest prefecture in Japan, by area, but at the same time Kagawa is called the "Udon Prefecture" thanks to its famous sanuki udon. Aside from Kotohiragu Shrine and Ritsurin Garden, the prefecture's small islands are popular, and Kagawa is full of unique destinations, like Angel Road. They say that if you lay eyes on Zenigata Sunae, a huge Kagawa sand painting, you'll never have money troubles ever again.

-

-

-

KYUSHU

VIEW MORE

Located in the most southwestern part of Japan, Kyushu (九州) is an island of 7 prefectures: Fukuoka, Saga, Nagasaki, Kumamoto, Oita, Miyazaki, and Kagoshima. The island's unique culture has been influenced by Chinese and Dutch trade, along with missionaries coming in through Nagasaki's port. Modern-day travelers love the lush natural scenery and fresh food, plus the natural hot springs found all throughout the area (thanks to volcanic activity)!

-

FUKUOKA

VIEW MORE

Fukuoka Prefecture has the highest population on the southern island of Kyushu, with two major cities: Fukuoka and Kitakyushu. Thanks to growing transportation networks, Fukuoka is more accessible than ever, and so are the many local attractions. On top of historical spots like Dazaifu Tenmangu Shrine, travelers shouldn't miss Fukuoka's food scene, with motsu nabe (offal hotpot), mentaiko (spicy cod roe), and famous Hakata ramen―best eaten from a food stall in the Nakasu area of Hakata. Plus, it's full of all sorts of destinations for travelers, like trendy shopping centers, and the beautiful nature of Itoshima and Yanagawa.

-

KAGOSHIMA

VIEW MORE

Kagoshima Prefecture played a major role in Japan's modernization as a backdrop for famous historical figures like samurais Saigo Takamori and Okubo Toshimichi, who pushed Japan out of the Edo era and into the Meiji. Because of that, Sengan-en Garden is just one of many historical destinations, and when it comes to attractions Kagoshima has plenty: the active volcano of Sakurajima, popular hot springs Ibusuki Onsen and Kirishima Onsen, World Heritage Site Yakushima Island, even what Japan calls the "island closest to heaven," Amami Oshima. Kagoshima might be found on the very southernmost tip of the southern island of Kyushu, but there's plenty to see.

-

-

-

OKINAWA

VIEW MORE

The island chain of Okinawa (沖縄) makes up the southernmost tip of Japan, which is why it's also the most tropical area in the country. Thanks to a history of independence and totally distinct political and cultural events, Okinawa has a unique culture, and remnants of the Ryukyu Kingdom are still visible all over the islands. Food, language, traditional dress, it's all a little different! It's also said to be the birthplace of karate.

-